Resource context and authorship

This resource is a press release from Catella Investment Management GmbH (CIM), an independent real estate investment advisor and subsidiary of Stockholm-based Catella AB. It summarises findings from the “Catella Residential Market Overview Q1/2025”, which analyses residential market indicators across 59 cities in 16 European countries. The release includes commentary from Dr. Lars Vandrei, Head of Research at CIM. The document is presented as a marketing release for information purposes and explicitly notes it is not investment advice.

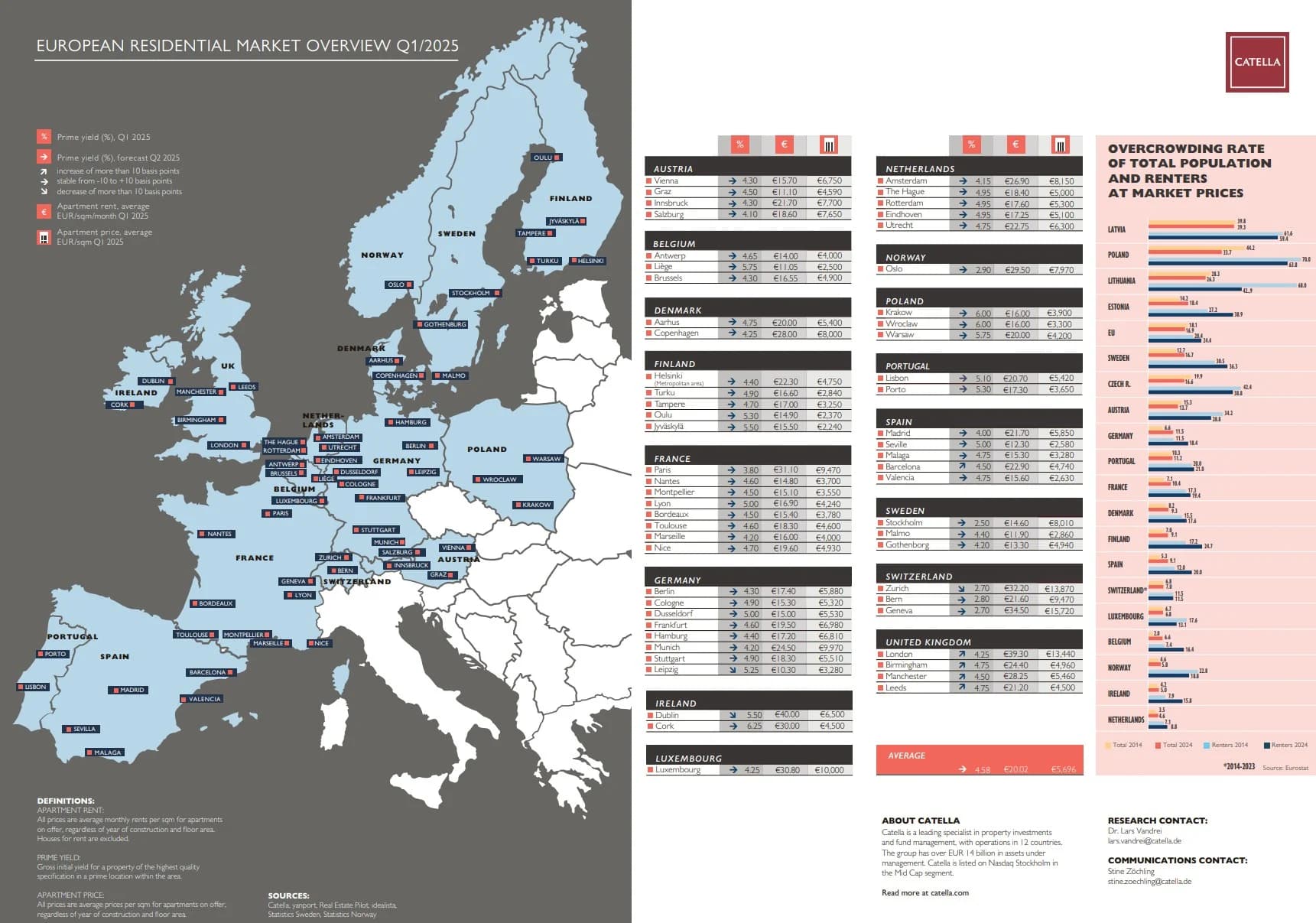

Headline indicators across Europe

The overview describes a continued tightening of housing supply, linking persistently low levels of new construction and high demand to rising rents and increasing overcrowding in rental housing. For Q1 2025, rents increased in 48 of the 59 cities analysed. The unweighted European average rent is reported at €20.02 per m² per month, representing a 2.4% increase compared with Q3 2024 across the same city sample. The publication also reports a mixed picture in purchase markets, with some areas showing moderate recovery while others continue to see slight price declines.

Rental market: levels and changes

The highest average rents in the study are in Dublin (€40.00/m²), London (€39.30/m²), and Geneva (€34.50/m²). Dublin is also cited as having the largest rent increase in the dataset (+€5.00). At the lower end, Leipzig (€10.30/m²), Liège (€11.05/m²), and Graz (€11.10/m²) are listed as the most affordable rental markets among the surveyed cities. Overall, the results are framed as evidence of strong rental demand across a broad set of European metropolitan areas.

Ownership market: prices, hotspots, and affordability

Condominium purchase prices rose in 31 of 59 cities, with an unweighted European average of €5,696 per m², described as a 0.9% increase versus Q3 2024. The highest prices are reported in Switzerland: Geneva (€15,720/m²), Zurich (€13,870/m²), and London (€13,440/m²). The most affordable ownership markets cited are the Finnish cities Jyväskylä (€2,240/m²) and Oulu (€2,370/m²). The largest relative increases since Q3 2024 are reported for Madrid (+11.9%), Gothenburg (+10.5%), and Copenhagen (+9.6%).

Yields and investment conditions

Average prime yields for multi-family residential properties are reported at 4.58% (unweighted), unchanged from Q3 2024 across the same markets. The lowest yields are listed for Stockholm (2.50%) and for Zurich and Geneva (2.70% each). Higher prime yields are cited in Cork (6.25%) and in Polish cities including Krakow and Wroclaw (6.00% each), as well as Warsaw (5.75%). The press release characterises Q1 2025 as a period of uncertainty, while noting “stabilized yields” alongside moderate price growth in parts of the market. 🇩🇪 Germany focus and overcrowding signal For Germany, rents are reported to have increased in all analysed cities, with Munich the most expensive rental market at €24.50/m², followed by Frankfurt (€19.50/m²) and Stuttgart (€18.30/m²). In the ownership market, Munich leads at €9,970/m², with Frankfurt (€6,980/m²) and Hamburg (€6,810/m²) next; Leipzig is cited as the most affordable among Germany’s eight largest cities at €3,280/m² and a prime yield of 5.25% (while Munich records the lowest yield at 4.20%). The special topic on overcrowding notes that although the EU-wide share of people living in overcrowded conditions fell slightly from 18.1% (2014) to 16.9% (2024), overcrowding among renters increased from 20.4% to 24.4% over the same period, with Germany’s renter overcrowding rising from 11.5% to 18.4% in ten years.