Overview of the Study and Its Origin

The bulletin is an Economic Research publication of the Banque de France, authored by Antonin Bergeaud, Jean‑Benoît Eyméoud and Thomas Garcia. The research team belongs to the Directorate General Statistics, Economics and International Business Surveys and the Directorate General Financial Stability and Operations. Published in the January‑February 2023 issue (Bulletin 244/3), the paper investigates the conversion of office buildings into residential housing in France, focusing on the impact of the Covid‑19 pandemic and the rise of teleworking.

How Teleworking Has Changed Office Demand

The authors document that teleworking surged after the 2020 health crisis, increasing the share of employees working from home from 3 % in 2019 to over 15 % in early 2022. This shift has lowered demand for office space, reducing office occupancy rates by 5.4 % since 2020. The reduction in office demand is identified as a negative shock to the commercial real‑estate market, with observed declines in prices and higher vacancy rates.

Current Scale of Office‑to‑Housing Conversions

Between 2015 and 2019, France recorded 10 474 office‑to‑housing conversions, creating 2.1 million m² of new residential space. These conversions represented 0.99 % of all new housing and 0.05 % of the total housing stock. Conversely, conversions of housing into offices accounted for 0.8 million m² (3.36 % of new office space). The conversion rate has risen modestly over the past decade but remains low.

Key Regional Variations

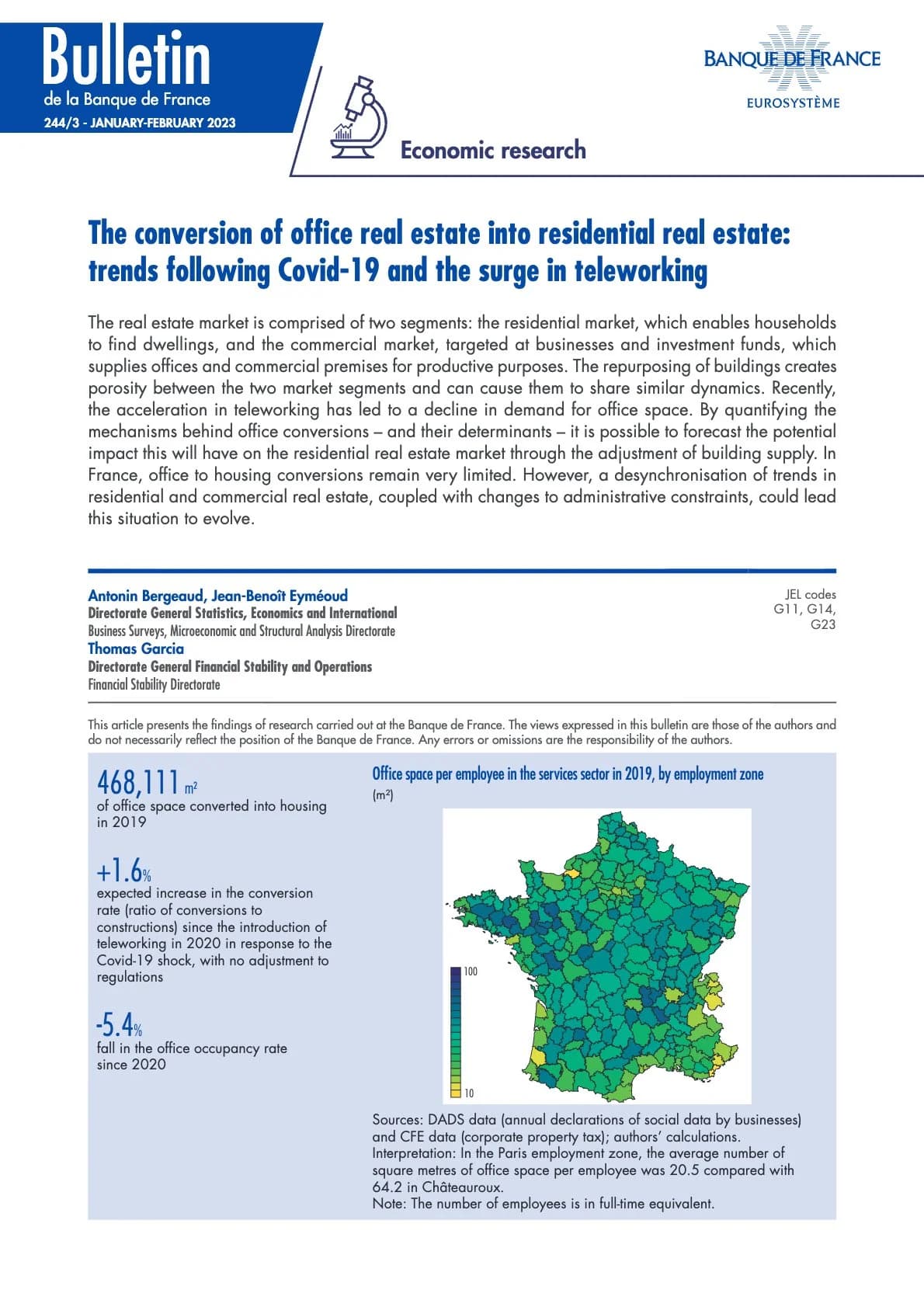

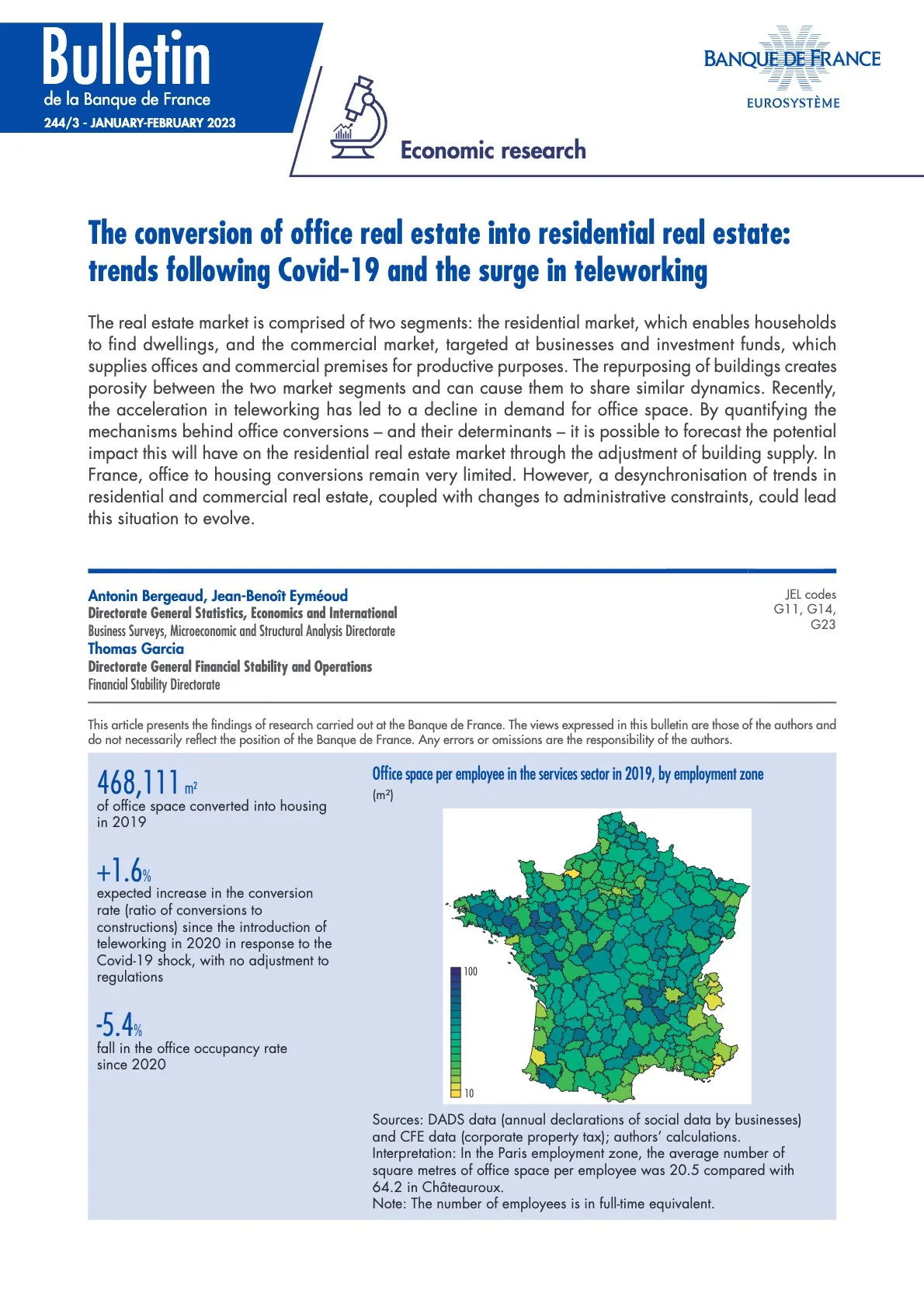

The conversion rate is uneven across employment zones. Higher conversion activity is observed in zones such as Paris, Poitiers, Roubaix and Reims, while zones like Menton, Sète and Fréjus show very few conversions. In 2019, the average office space per employee varied from 20.5 m² in Paris to 64.2 m² in Châteauroux, highlighting spatial constraints that influence conversion potential.

Drivers and Constraints of Conversions

The authors’ econometric model shows that lower office space per employee (i.e., less constrained office occupancy) positively affects conversion rates. Large office stock combined with limited housing stock also encourages conversions. However, relative prices of offices versus housing do not have a statistically significant impact. Strong regulatory and physical constraints—such as building structure, heritage preservation, and local planning rules—limit the speed and scale of conversions. The 2018 Elan Law offers some incentives, granting constructibility bonuses in towns lacking sufficient social housing.

Projected Impact of Continued Teleworking

Assuming teleworking rises from 3 % to 15 % of employees working from home two days per week, the model predicts a 5.4 % increase in office space per full‑time equivalent employee and a modest 1.6 % rise in the office‑to‑housing conversion rate. Given the already low baseline, the overall effect on housing supply is expected to be modest, and price impacts are likely marginal without regulatory reforms.

Sustainability Implications

Conversion of existing office buildings into residential units can lower carbon emissions compared with demolition and new construction, aligning with broader European sustainability goals. While converted buildings may have lower energy performance than new builds, life‑cycle analyses suggest they often emit fewer greenhouse gases over their lifespan. The study thus highlights conversions as a potential tool for greener urban development, provided administrative barriers are eased.

Outlook for Policy and Market Actors

The authors conclude that without targeted policy changes—such as streamlined approvals, incentives for adaptive reuse, and adjustments to zoning—teleworking alone will not dramatically reshape the French housing market through office conversions. Nonetheless, the identified modest upside, combined with environmental benefits, suggests that policymakers and developers should consider conversion projects as part of a diversified strategy for sustainable housing across Europe.