Overview of the Research Publication

AEW’s research titled “Increase In Conversions Expected To Benefit European Office Market Recovery” is authored by Irène Fossé, a noted analyst in European real‑estate trends. The study provides a comprehensive analysis of office market dynamics across 61 European sub‑markets, focusing on vacancy trends, conversion activity, rental growth, and projected returns up to 2029. It also examines the impact of generative AI on office employment and the sustainability implications of office‑to‑residential conversions.

Office Vacancy Trends and Outlook

In Q1 2025, overall European office vacancy stood at 9 %—up from the pre‑COVID level of 5.7 % in 2019—but is expected to decline to around 7 % by 2029 as conversion activity accelerates and new supply slows. CBD vacancy peaked at 5.6 % versus 10.6 % in non‑CBD sub‑markets, with a recent 120‑basis‑point rise in CBD vacancies. The study projects a gradual rebalancing of supply and demand, aided by a modest 0.7 % annual new office stock growth over the next two years, well below the historical 1.3 % rate.

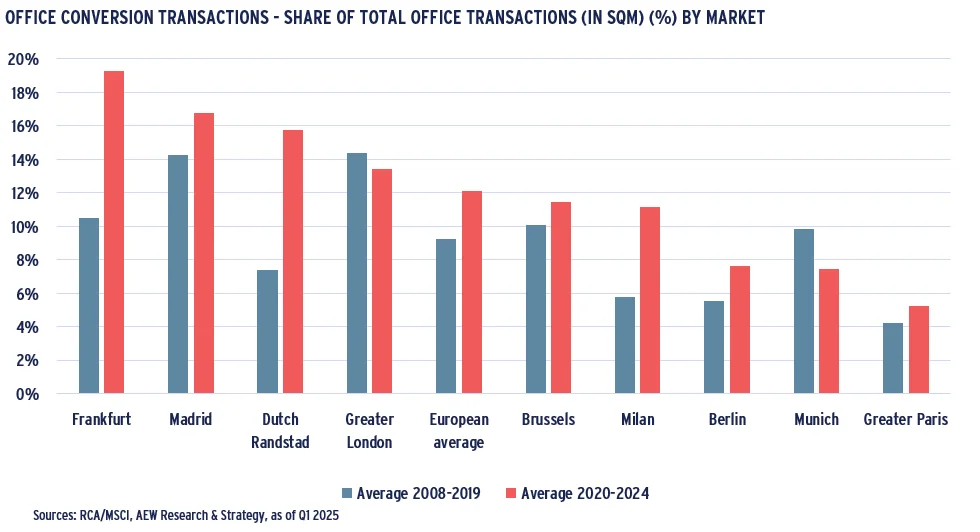

Rise in Office‑to‑Residential Conversions

Office conversions accounted for more than 30 % of total office transactions in the first four months of 2025, up from 17 % in 2024 and far exceeding the post‑GFC average of 8 %. Frankfurt and Madrid lead the conversion share, while London and Munich show lower activity. Conversions are driven by high vacancy, regulatory flexibility, and sustainability incentives, as repurposing existing structures reduces lifecycle carbon emissions compared with demolition and new construction.

AI’s Positive Influence on Office Employment

The report highlights that generative AI is projected to create higher‑value jobs while automating routine tasks, resulting in a net positive effect on office employment. AI‑related roles are expected to grow from 0.3 % of total office jobs in 2024 to 3.2 % by 2040, adding roughly 1.2 million positions. Cities with strong finance, insurance, and IT sectors—London, Paris, and Frankfurt—rank highest in AI benefit indexes.

Rental Growth and Yield Projections

Average prime rental growth for 2025‑29 is forecast at 2.8 % p.a. across all covered markets, with CBD sub‑markets slightly ahead at 3.5 % p.a. versus 3.3 % p.a. in non‑CBD areas. Yield spreads between CBD and non‑CBD markets are expected to narrow, with CBD yields peaking at 4.7 % in 2025 and compressing by 20 bps, while non‑CBD yields peak at 6.1 % and compress by 30 bps. Total return expectations average 9.4 % p.a., ranging from 12.7 % in London City to a low of 8.2 % in London West End. Non‑CBD sub‑markets with higher income yields are projected to deliver 10.4 % p.a., outperforming CBD averages.

Sustainability Benefits of Conversions

Office‑to‑residential conversions align with European climate goals by extending the functional lifespan of existing building stock, lowering embodied carbon, and reducing construction waste. The increased regulatory focus on lifecycle emissions makes retrofitting more attractive than new builds, supporting the EU’s broader sustainable housing agenda.

Investment Sentiment and Liquidity Outlook

European managers exhibit a markedly more optimistic view of office assets than their US counterparts. Over 40 % anticipate a positive capital value increase for offices within the next year, and liquidity is expected to improve as investors perceive the market bottoming out. Despite a 53 % drop in 2024 office transaction volumes versus the 15‑year historic average, the study forecasts a gradual recovery driven by conversion activity and improved sentiment.

Regional Highlights and Risks

While most markets are projected to see vacancy reductions, Frankfurt, Hamburg, and Brussels may experience persistent high vacancy. Milan, Frankfurt, Amsterdam, and Barcelona face vulnerability due to elevated vacancy and anticipated stock growth. Conversely, Brussels may see negative stock growth thanks to conversion offsets. London, Paris, and Frankfurt remain the primary beneficiaries of AI‑related productivity gains.

Key Takeaways for Sustainable Housing Stakeholders

- Office conversion activity is a major driver of sustainable urban housing supply, expected to exceed 30 % of office transactions in 2025.

- Conversions reduce carbon footprints by avoiding demolition and new construction, aligning with EU sustainability targets.

- Rental and yield dynamics suggest that non‑CBD sub‑markets, often more affordable, will deliver higher total returns, supporting diversified investment strategies.

- AI‑induced employment growth reinforces the economic viability of repurposing office spaces for mixed‑use and residential uses. Overall, the AEW research presents a detailed, data‑rich outlook indicating that office‑to‑residential conversions will play a pivotal role in Europe’s post‑COVID office market recovery and sustainable housing development.